Risk Assessment and Determination of Audit Topics

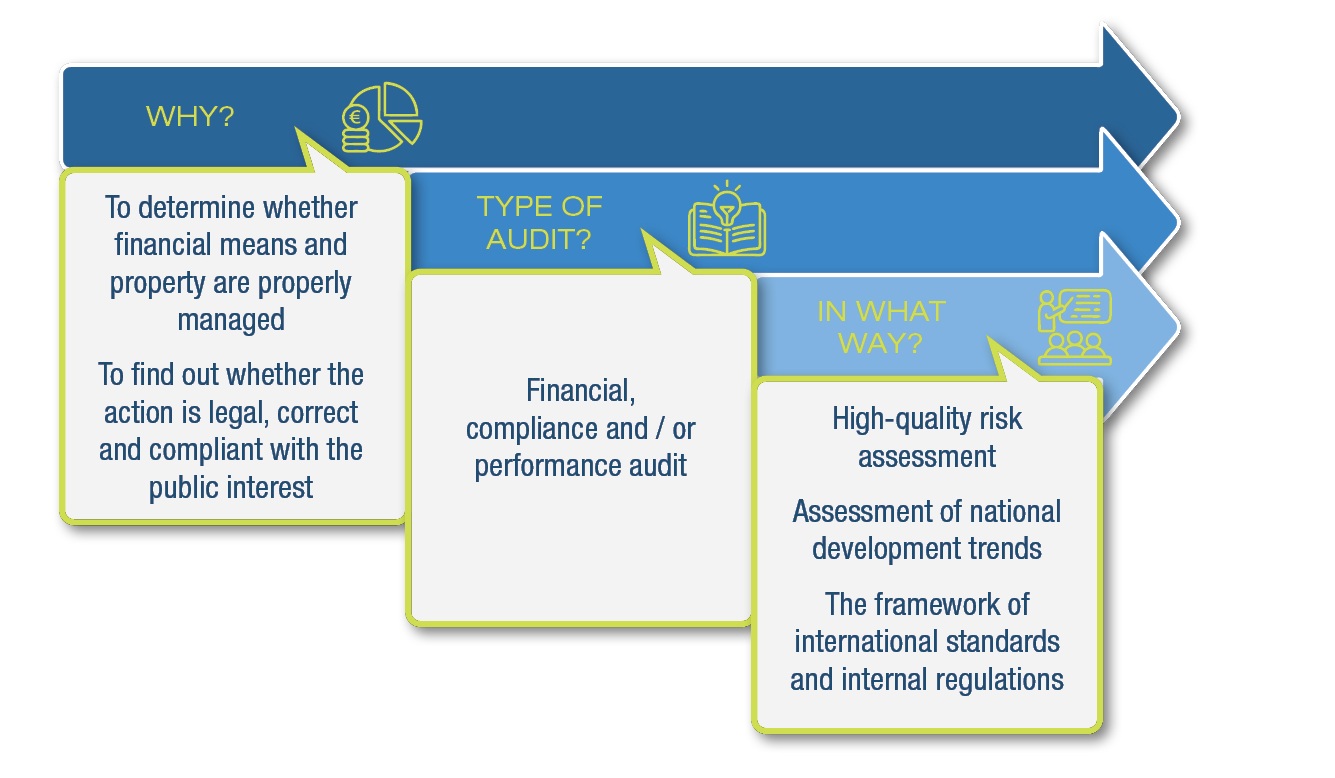

The purpose of the activity of the State Audit Office of Latvia is to find out whether actions with the financial means and property of a public entity are legal, correct, efficient and compliant with the public interest. To accomplish this, the State Audit Office conducts financial audits, compliance audits and performance audits. The State Audit Office of Latvia determines the topics for compliance audits and performance audits based on a risk assessment and plans its activities in such a way that planned audit topics meet the most pressing challenges as much as possible. To identify these risks, the State Audit Office of Latvia performs an assessment of public policy areas with the aim of focusing on those audit topics which, when audited and given recommendations for their arrangement, would have the greatest potential for social and economic impact.

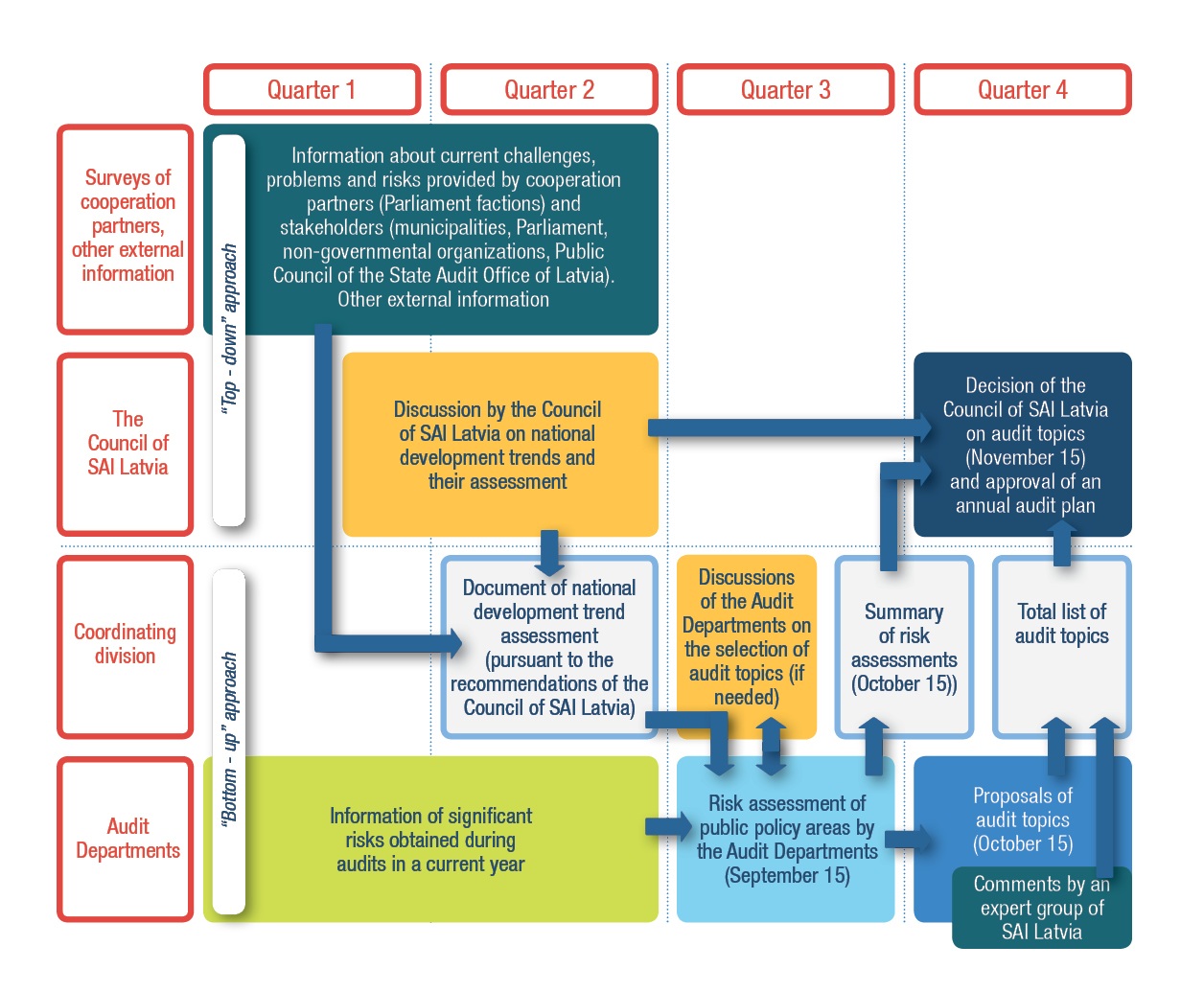

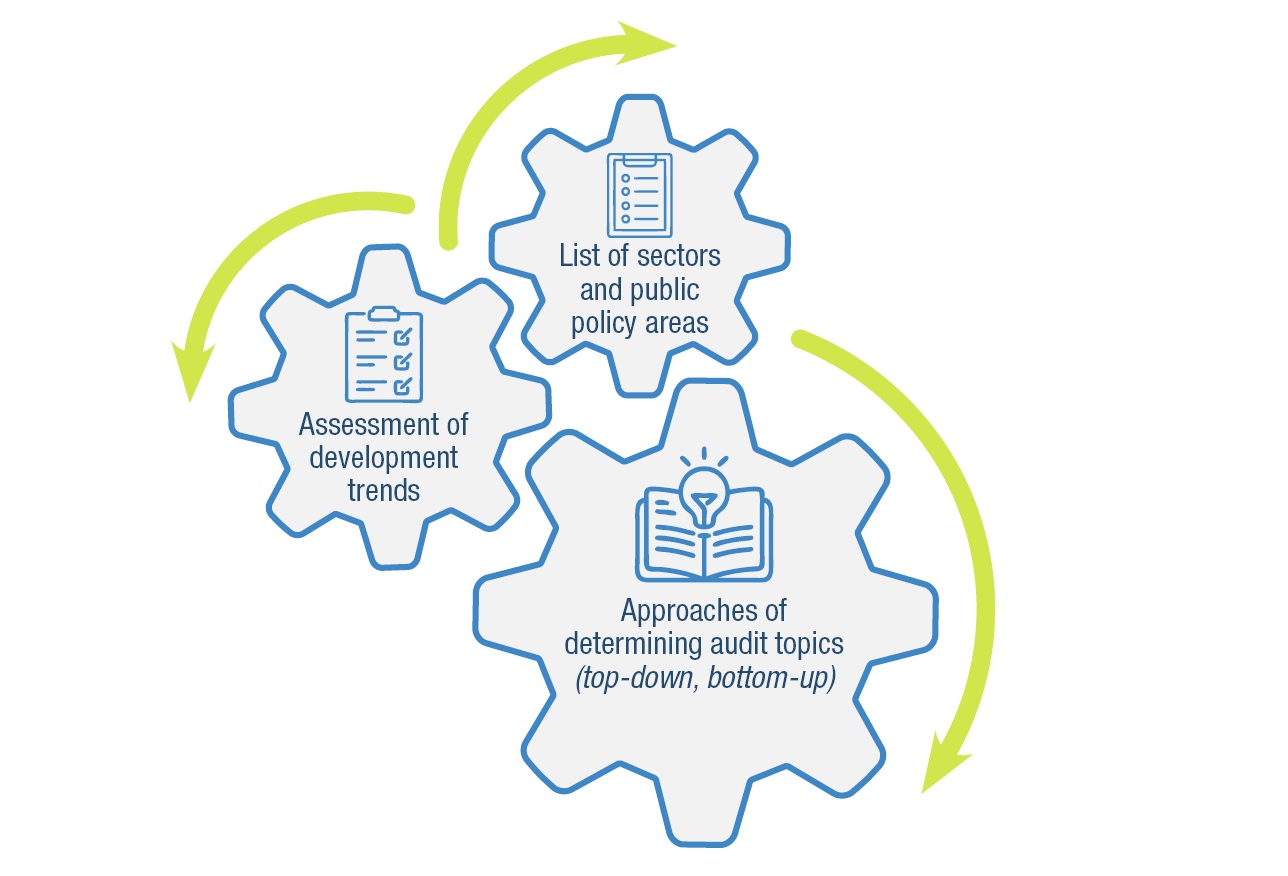

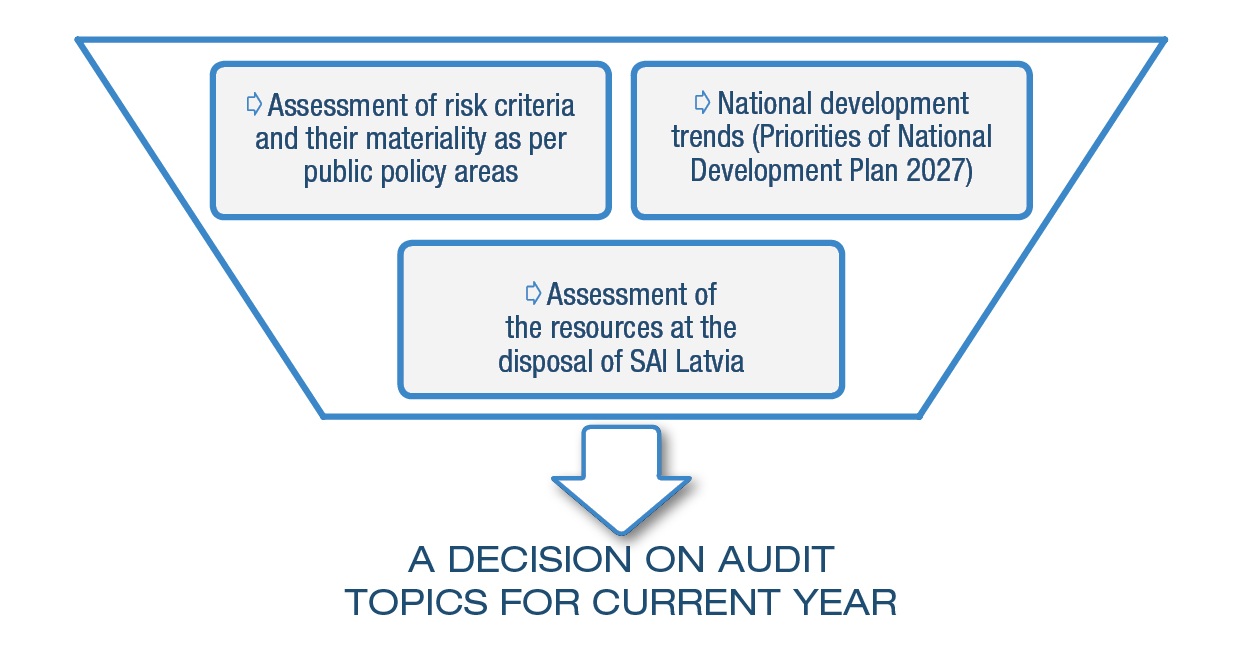

In risk assessment, the State Audit Office of Latvia complies with both the requirements of international auditing standards and the internal regulatory framework, which stipulates that in the process of selecting audit topics, an assessment of national development trends (performance indicators of policies and their indicators), risk assessment of public policy areas and proposals of audit topics are elaborated.

The Council of the State Audit Office of Latvia uses an assessment of national development trends when deciding on potential medium-term auditing directions. The assessment corresponds to the priorities and focuses defined in the national development plan. The assessment compares the baseline and actual values of the indicators of the achieved performance indicators with the planned target values, namely, it is analysed whether they are aimed at achieving the target values. Special attention is paid to those trends and indicators that are contrary to the intended target values.

In addition, the assessment of development trends includes the challenges outlined by cooperation partners (Parliament factions, non-governmental organizations, social partners, municipalities), as well as the assessment of social and economic risks by international organizations. Thus, a systemic assessment of the entire auditing environment is achieved.

For assessing the risks of public policy areas in accordance with the international standards of supreme audit institutions (ISSAIs), the State Audit Office of Latvia discusses and drafts a list of applications for audit topics. The audit topic selection process is structured and documented. According to the list of public policy areas, risk assessment of public policy areas and annual assessment of applications for audit topics are provided. Thus, the State Audit Office of Latvia applies both methods of determining audit topics, that is, by assessing the country’s development trends (top-down) and by using the knowledge and experience accumulated in the respective audit department (bottom-up).

A sector is a competence of state administration under the control of the respective audit department, which is based on the institutional division of state administration. A public policy area is a classification unit of sector determined according to the essential functions of the sector, the regulations of state institutions, development planning documents and the auditors’ experience. Divisions into sectors, public policy areas and an annual risk assessment of public policy areas are developed by the audit departments of the State Audit Office of Latvia taking into account 1) possibilities of using audit methods, 2) the specifics of the sectors, 3) the division of budget programs, 4) key groups of government functions, 5) any specific conditions of a concrete period, e.g., expenditure for overcoming new challenges, as well as other considerations based on the auditor’s experience.

The audit departments carry out a risk assessment of public policy areas of the sector every year to ensure that audit topics are relevant to the public. A risk assessment is a process of obtaining a representative and qualitative set of risk observations for each area. A risk assessment of public policy areas is compiled as per sectors depending on specific needs. The risks of each area are assessed according to 12 criteria, which are divided into four groups. Each risk criterion is given a qualitative assessment in points (from 0 to 5 points) in accordance with an assessment determined by the State Audit Office of Latvia, as well as the materiality of the criterion, which is determined by the specific conditions of the concrete public policy area. For example, in public policy areas where essential services are provided to the public, the materiality of the risks of beneficiary satisfaction (complaints) will be higher than in other areas. The overall risk assessment as a product of the assessment and materiality of all criteria is expressed as a percentage from 0% (the lowest possible risk) to 100% (highest possible risk). The State Audit Office of Latvia has determined that high-risk public policy areas are those with a risk rating above 60%. They are usually around 20% of all 112 public policy areas.

The State Audit Office of Latvia has defined the following risk criteria for public policy areas, according to which the auditors provide a high-quality assessment which has been broadly discussed:

- Whether there are risks that the resources allocated to an area are insufficient and will not be used according to the targets;

- Whether information on the area’s expenditure is sufficient and of high quality;

- Whether information on the area’s performance indicators is available and updated regularly;

- Whether the governance of an area (centralised, decentralised) affects the risks;

- Whether the planned and implemented reforms pose risks for the implementation of the tasks set in the area;

- Whether information is available about the service recipients of the area;

- Whether the established information systems and databases meet the needs and allow to obtain reliable information;

- Whether the human resources available in the area are sufficient and adequate to ensure the performance of the area’s tasks;

- Whether there is sufficient and high-quality infrastructure (buildings, equipment, technologies) to ensure the implementation of policies and tasks in the area;

- Are there available studies and audits that assess the possibilities of improving the area;

- Whether the current affairs of the area have been revealed in the mass media;

- Whether submissions and complaints have been received.

Based on the overall risk assessment of public policy areas, its changes, as well as additional assumptions related to the workload of auditors and the sequence of audits, the audit departments propose potential audit topics. The final decision on the next year’s audits is taken by the Council of the State Audit Office of Latvia taking into consideration the extent of achievement of medium-term national development goals, the information obtained during current financial audits and the proposals submitted by the audit departments. Following current events, the Council of the State Audit Office of Latvia can make a decision on postponing audits or other amendments to a work plan, for example, by including more current audit topics.